14th February 2023

Need help getting on the property ladder? Family Assist Mortgages can provide a way for family members to help the younger generation buy a property without the need for a deposit.

.jpg)

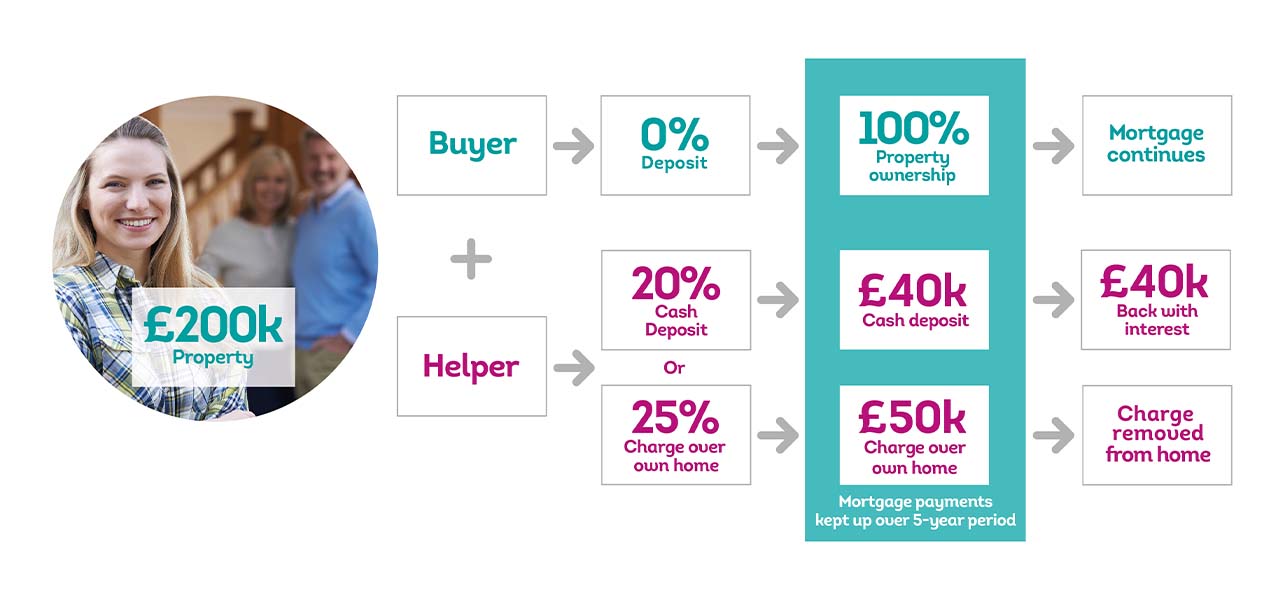

A Family Assist Mortgage (sometimes called a Family Mortgage) allows a borrower to use the security provided by their family to help them buy a home. This security usually comes in two forms; either a lump sum which sits in a savings account earning interest, or a percentage charge on a family member’s property.

This security allows borrowers to borrow 100% of the property value with no deposit.

Family Assist Mortgages aren’t just for first-time buyers, they’re for everyone who might be struggling to save up for a deposit. If for whatever reason, a buyer finds themselves looking to purchase a home without a substantial enough deposit, they can get help from their family.

Family Assist Mortgages are also good for those whose circumstances mean they potentially face the prospect of not being able to afford their current home. In many cases, a Family Assist Mortgage can allow family members to help make staying a reality.

With house prices at an all-time high, for many, saving up for a deposit is becoming an increasingly unrealistic prospect – especially given the fact that average wages haven’t kept up with house prices. On average, full-time employees could expect to spend around 9.1 times their workplace-based annual salary on purchasing a home; an increase since 2020, when it was 7.9 times their workplace-based annual earnings. (Source: Office for National Statistics)

This is where Family Assist Mortgages come in. This mortgage means families can help their loved ones get into an inaccessible market.

For many, simply gifting and receiving a deposit isn’t financially viable. With a Family Assist Mortgage, a family can either deposit money into a savings account or place a charge over their property. These amounts must usually be a minimum percentage of the new property’s value, so it’s important to check this before progressing further.

If the helper is using their savings, the lender will then hold the funds for a period of time (usually five years), where the money will earn interest. If a charge is put over a property, the lender will hold this charge for a period of time (again, usually five years).

Usually, after the period, for the family to be fully released from their commitment and responsibility for the mortgage, an affordability assessment will be conducted to prove that the Buyer can afford to take on the mortgage by themselves.

As with most financial products, the terms offered will depend on many factors including the applicant’s financial background.

For The Vernon’s Head Start Mortgage, the maximum loan amount is £500,000 and the minimum is £125,000.

Many lenders offer their own versions of a Family Assist Mortgage. So, whether you’re helping a buyer or getting help, it’s good to speak to a specialist before making any decisions.

If you have a family member who would be willing to use their capital as security, then it might be worth asking to achieve your property dreams. If you’d like to find out more about the Vernon’s Head Start Mortgage, please get in touch.